It’s the year 2007, you’re riding on the boom of the world economy, specially the finance industry, and you have just purchased a house on mortgage. With it came the purchase of various furniture & fittings, consumer durables and electronics on your credit card. In 2008 the Lehman Brothers crisis takes place and you are out of your job. Now you wish you had purchased, at the same time, an Accident, Sickness and unemployment (ASU), Income Pro-tection, insurance product.

However, before we go ahead to explain what is the best way to purchase ASU Insurance, let’s first explain what ASU Insurance is all about.

What is ASU Insurance?

ASU insurance is a monthly premium payment, Income Protection insurance. It is intended to enable you to continue to pay your mortgage payments (such as a home loan), unsecured loan repayments (such as personal loan) and rent payments in case of your inability to work due to accident, sickness and redundancy, over a specified period.

Key Features

- This type of insurance can be taken with initial waiting / gestation period of 30 to 90 days.

- Generally, the maximum period this type of insurance will cover you would be 12 to 24 months.

- The maximum amount of insurance cover allowed would be your monthly outgoings and mortgage or 60 % to 75% of your income, whichever is the lower.

- Unless you cancel the insurance or make a claim the ASU cover rolls over month by month and is renewable at the end of the specified time.

- Mortgage payments

- General outgoings

- Unemployment insurance (U); or

- Accident & Sickness insurance (AS); or

- Accident, Sickness and unemployment insurance (ASU)

- The Insured is over the 18 and under 65 years of age. (Please note usually the insur-ance company stops taking any fresh ASU insurance 5 years prior to the maximum eligibility age)

- The Insured should be a permanent resident of UK

- The Insured should not have been absent from work on any earlier occasion on ac-count of illness or accident, subject to those already highlighted by the applicant and agreed by the insurer.

- The Insured has been working 16 hours a week within UK for the previous 6 months

- Any pre-existing illness, subject to those already highlighted by the applicant and agreed by the insurer prior to providing the cover.

- Any self inflicted injury

- Any injury caused due to consumption of alcohol, tobacco or drugs

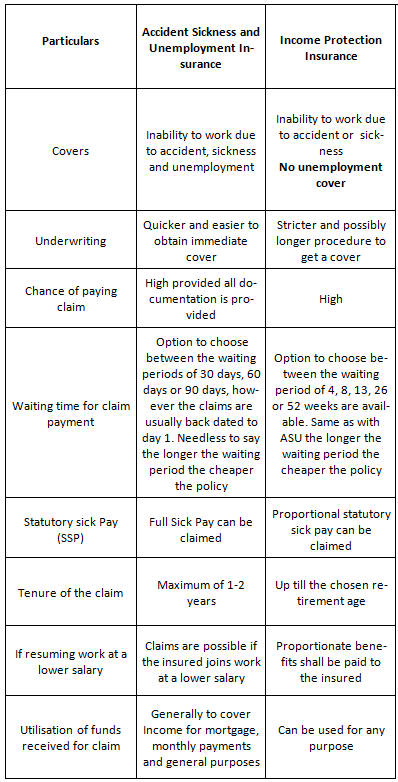

There is another type of Income Protection insurance, Permanent Health Insurance (PHI).

PHI is similar to ASU and also can cover your mortgage and other monthly expenses. However, there are two major differences between them; firstly PHI does not provide redundancy cover and secondly it is usually taken for a longer period in contrast to ASU.

The table below gives a basic understanding and shows the main differences between ASU and PHI;

Buying a policy: (All you need to know)

To understand how to purchase an Income Protection Insurance product, let us have a closer look at the main attributes of which might help you to decide which one to buy - Accident, Sickness and Unemployment Insurance (ASU) or, Permanent Health Insurance (PHI)?

You need to identify your income requirements according to the various factors and then choose the plan which best suits your needs. Depending upon your circumstances e.g. your age, financial situation, dependency of family members upon your income, personal health condition, duration of cover, etc. one can choose between an ASU or PHI.

Age: Though it is generally cheaper to get any personal insurance at a younger age as the insured is likely to be in better health when young. If the applicant is contemplating a new ASU or PHI, it may be preferable for them to take PHI when young and an ASU when older. If at a younger age the insured is not confident about their employment stability then he or she can take separate unemployment cover for his or her mortgage, loan and monthly pay-ments.

Health habits: Healthy habits such as yoga, exercise, eating meals on time, eating healthy food and avoiding junk food, non consumption of tobacco, alcohol or drugs all help to keep you healthy and less prone to sickness. All insurance providers will require a declaration from the applicant regarding health, etc, and it is on the basis of the declaration that the cover is provided. When a claim is made a formal check will be made of health and income against the information provided by the insured. It is absolutely essential the applicant pro-vides honest and accurate information when taking up any insurance.

Dependency of Family members: If you are the only earning member of the family and you have dependents it is advisable to take a PHI, or a longer term Accident and Sickness (AS) together with unemployment insurance for mortgage, loan and regular payments. If your family members are not dependent and if they can assist in supporting you in case of any out of work problems, then it may be preferable to take ASU as its generally cheaper and can be for a known duration.

Personal Health Condition: If you are a diabetic, suffer from hypertension or have high cholesterol etc. it is very likely the PHI premium would be much higher than ASU.

Sick Pay: Before buying ASU or PHI it is important to know what financial support you are entitled to from your employer. Some employers have built in packages referred to as occu-pational or company schemes; these will generally pay a persons salary for a certain period. If such a scheme is not built into your pay package employers have to, at least, provide sta-tutory sick pay (SSP).

SSP is provided under the following circumstances:

- You are categorised as an employee (including agency workers)

- Your before tax earning is a minimum of £112 per week

- You Inform your employer of your sickness in the stipulated timeframe

- You have not been to work for a continuous period of 4 days (including non-working days)

PHI generally provides cover for a longer duration and the sum received under PHI can be used for any purpose. If you are young and healthy, smoker or non smoker, and if you are considering ASU, PHI with added Unemployment cover, it is advisable to take your time, check all of the benefits of each and compare them with your employer benefits, your lifestyle requirements and your dependant’s ability to offer support in the event of you be-ing unable to work. If you are in any doubt, you should seek expert advice from a regulated Independent Financial Adviser.

The major differences between the products are how they pay out and why. So one has to look at the circumstances for which you want to be covered and is it worth paying any addi-tional premiums.

Different Distribution Channels available:

There are various distribution channels available:

- Independent Financial Advisors or IFAs:

There are Independent Financial Advisors or IFAs regulated by The Financial Conduct Authority (FCA) who are qualified and able to recommend appropriate product(s) af-ter carrying out a needs analysis. - Brokers: With brokers, one may get the advantage of better comparison or a broader range of products, help with policy servicing and even claim assistance.

- Aggregators/Comparison Sites: These companies have grown in popularity and pro-vide, via the internet, unbiased comparisons of products across insurance providers. Prospective customers can compare the products themselves and purchase directly online through the aggregator websites and may also get information on policy ser-vicing and claims.

- Bancassurance: Some banks have partnered with some insurance companies to source the Insurance products for their customers.

- Single Tie: Some distributors and well known brands have gone ahead in an exclusive agreement of sale of a single company product under this agreement. The products for this channel are usually fully underwritten in advance with simplified processes. Pricing is usually higher than that of the IFAs though due to higher commissions and better business mix.

- Direct: However, if premium is the determining factor, then purchasing the policy di-rectly from the company’s website may be a preferred choice. Choosing that option, like buying from an aggregator/comparison site, you will have to complete the entire application yourself, including Direct Debit Instructions. Most direct insurance providers offer the same level of support, covering administration, claims and renewals, etc., through either their own resources, or using a third party administration company.

You could purchase the product directly from an insurance company or from a broker online or in person depending upon your knowledge of the product and your comfort. However online purchase or a direct purchase may be cheaper.

Globally, the trend for online insurance purchase has increased over the years. With inter-net usage becoming ever more popular, there has been a change in the trend of insurance purchase and customer preferences around buying insurance products. According to a re-port from the Boston Consulting Group (BCG), customers currently compare online but pre-fer to purchase offline. However, it’s a fast changing trend like the banking industry. The online sale is sometimes very beneficial to the customer as the distribution cost are likely to be lower and can work with economies of scale. There has been a huge influence of social media, e.g., Facebook, Twitter, etc., on online sales for insurance policies.

Now, the insurance companies also have different products for different distribution chan-nels. The distributors, i.e. the IFAs, Agents as well as Brokers, have started to recognise and identify their power to influence both the designing of the product as well as the price along with underwriting strategy to fit the specific distribution process.

Choosing the correct insurance cover that meets your personal needs and situation contin-ues to need proper, detailed and clear thinking; who to buy it from, where to buy it from, duration; short, medium or long term and Cover type; Accident, Sickness, with/without Un-employment (AS/U), Permanent Health Insurance (PHI); Advice or no advice.

The most important consideration is to have it in place when you need it and not wish that you had when the problem occurs.